Energy and renewable sources: what is the current status?

17 March 2020

The relentless growth of renewable energy sources continues…

The Renewable Energy Policy Network for the 21st Century (Ren21) periodically publishes data and statistics on the market, industry, investment and policies regarding renewable energy sources worldwide. These data are illustrated and analysed in the “Renewables 2019 Global Status Report“, now at its fifteenth edition. The publication of the report therefore allows us to draw a picture of the current situation of worldwide renewable sources, a constantly evolving and changing sector.

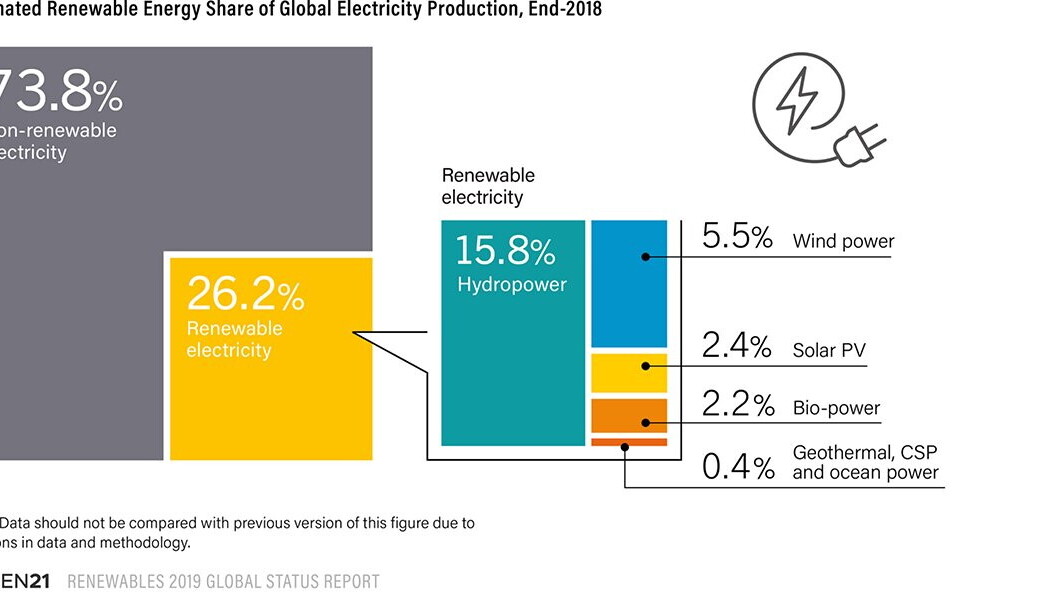

Analysing the Report’s data for 2018, it can be seen that the past few years have been marked by record growth in renewable sources, particularly solar and wind power. The most significant growth in renewable energy has been in the electricity sector. During last year, in fact, installed power increased as never before, adding approximately 181 GW more and bringing the world total to 2,378 GW, equivalent to an increase of 8.2% over 2017. According to the report, renewable sources, which at the end of 2018 accounted for 30% of world electric power generation capacity, were able to cover 26.2% of the demand for electricity, and hydropower on its own providing 15.8% of renewable energy (see image below). These results are due both to policy initiatives, which set new targets to be achieved, and to falling costs and the progress of renewable technologies. About 100 GW of photovoltaic power was installed in 2018, representing 55% of the new renewable capacity added in 2018, followed by wind (28%) and hydro (11%) power. Overall, renewable energy has increased to account for over 33% of the world’s installed electrical capacity. By 2018, more than 90 countries had installed at least 1 GW of generation capacity, while at least 30 countries had a capacity of more than 10 GW.

Renewables 2019 Global Status Report

With regard to building heating and cooling, in 2018 renewable energy sources covered around 10% of global energy demand in this sector, but their growth remains slow due to the persistently limited political focus on this sector. In 2018, only 47 countries had set targets for integrating renewable energy sources into the heating and cooling of buildings, while the number of countries with regulatory policies in the sector fell from 21 to 20. During 2018, especially in Europe, there was an increase in integration of renewable sources into district heating and cooling systems and the use of hybrid systems for production of domestic hot water.

Where they exist, policies to increase the use of renewable energy in buildings and industry are often integrated with energy efficiency policies: the choice to use renewable energy technologies is therefore accompanied, for example, by reductions in energy consumption and compulsory use of efficient lighting or luminaires. Renewable heat sources – geothermal, biomass and solar thermal energy – can help decarbonise both buildings and industry. The expansion of renewable energy in heating and cooling – an important end use of energy in buildings and industry – represents an opportunity for policy makers seeking to decarbonise or transform their energy sectors.

In conclusion, although there is a huge potential for renewable energy, and technological innovations are available in the building heating/cooling sector, use of renewable sources is still marginal in this sector.

In the transport sector, too , use of renewable sources is limited to a small proportion of liquid biofuels (ethanol and biodiesel), which account for 3% of consumption. Oil is, in fact, the predominant source covering 95.9% of final energy consumption in the transport sector.

The main entry points for renewable energy in the transport sector are: the use of biofuels blended with conventional fuels, as well as higher blends including 100% liquid biofuels; natural gas vehicles converted to run on biomethane; electrification of transport vehicles, through the use of hybrid vehicles, battery electric vehicles, hydrogen vehicles, synthetic fuels and electro-fuels, provided the electricity is generated from renewable sources.

Obstacles to electrification in the transport sector include the relatively high cost of purchasing electric vehicles, limited battery life and lack of battery charging infrastructures. In most developing countries, there is also a lack of a high electricity supply which reduces the attractiveness of using electricity for transport.

No less than 80% of countries recognised the key role of the transport sector in mitigating CO2 emissions by including transport in their Intended Nationally Determined Contribution (NDCs) under the Paris Agreement of December 2015 (COP21). The 2018 IPCC Special Report also included transport in its call for urgent action to increase climate change mitigation. However, despite this awareness, many governments do not have a transport decarbonisation strategy. Such strategies should include greater integration of renewable energy (both through renewable fuels and renewable electricity) and reduction of overall transport needs; a shift to more efficient modes of transport, such as public transport, cycling or rail; and improved vehicle technologies.

Renewable successes

The evolution of renewable energies over the past ten years has exceeded all expectations, in fact, overall installed capacity and energy production have increased significantly and there has been a trend towards increased investment and policies in favour of renewable energies since the early years of this century. The energy and economic crises of recent years and the growing attention and commitment to climate change mitigation have been the driving force behind this rapid development, exceeding all growth forecasts. In addition, some pioneering countries in the renewable energy sector, such as Germany, Denmark, Spain and the United States, have laid the foundations for the first technological advances, triggering exponential growth in the renewable energy market.

Advances in technology and the rapid development of renewable energies, especially in the electricity sector, have amply demonstrated their potential. Today, renewable technologies are seen not only as a means of improving energy security and climate change mitigation and adaptation, but are also increasingly recognised as an investment that can provide direct and indirect economic benefits, for example by reducing dependence on imports of traditional fossil fuels. They also contribute to improvement of local air quality, promote access to energy in rural areas and help to create new jobs.

The sector in which the greatest growth was recorded was electricity generation.

Hydroelectricity, which covers 48% of renewable capacity, is confirmed as the prime renewable technology in terms of installed capacity. During the course of 2018, 20 more GW were installed, with a total capacity at year-end of 1,132 GW. China, Brazil, the United States, Canada, Russia and India, who together cover 60% of global hydropower, were confirmed as the top countries for installed capacity.

As far as photovoltaics are concerned, 100 GW were installed during 2018, thus reaching 505 GW of power worldwide. For the sixth consecutive year, Asia has eclipsed all other regions for new installations: suffice it to say that in 2018 new installations in China, whose installed PV power grew from 0.3 GW in 2009 to 176 GW in 2018, accounted for about 45% of the world total. The top five domestic markets – China, India, the United States, Japan and Australia – accounted for around three-quarters of installed capacity in 2018. Despite these figures, the growth todate reflects only a small part of the enormous potential of the photovoltaic market: many areas such as Africa, the Middle East, South-East Asia and Latin America have yet to start using the high potential available to them.

Equally noteworthy was the growth of wind power, whose installed capacity reached 591 GW, with 51 more GW installed in 2018. For the wind power market,2016 was another good year, since cost reductions and improvements in existing technologies have made wind power competitive in an increasing number of markets. For the eighth consecutive year, Asia remains the largest market, accounting for about half of the installed capacity during the year, followed by Europe and North America. Eighty-four percent of the world’s wind power is located in only 10 countries: China, United States, Germany, India, Spain, United Kingdom, France, Brazil, Canada, Italy.

Bioenergy (modern and traditional) is still the renewable energy source that contributes most to covering the world’s primary energy consumption, 12.4% to be exact. Traditional biomass is still widely used in developing countries: firewood, coal, agricultural residues and manure, burned in open fires, furnaces and cooking ovens. As far as modern biomass is concerned, solid forms are used more for heating and electricity production, while liquid biofuels provide power for the transport sector.

The growth of geothermal energy was more limited, however, and in 2018 it grew by only 0.5GW, reaching 13.3 GW of global installed capacity.

by Benedetta Palazzo

Sources: